- Home

- Our Offerings

- Partners

- Insights

- Contact Us

EU Omnibus Regulation - Old Wine in New Bottle or New Wine in New Bottle?

The European Union stands as a global leader in sustainability regulation, continually refining its approach to ensure environmental responsibility and corporate transparency. The EU Omnibus Regulation represents a watershed moment in this journey—an ambitious attempt to streamline existing sustainability frameworks while maintaining their effectiveness.This paper examines whether the Omnibus Regulation is simply “old wine in a new bottle”—a mere rebranding of existing regulations—or “new wine in a new bottle”—a genuinely innovative approach to sustainability governance. By analyzing its relationship with the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), and the EU Taxonomy for Sustainable Activities, we provide a comprehensive assessment of its impact on businesses within and beyond the EU.

This white paper examines the European Union’s Omnibus Regulation, which represents a pivotal evolution in the EU’s sustainability regulatory framework. By analyzing whether this regulation is merely a repackaging of existing rules or a genuine innovation, we provide stakeholders with crucial insights for strategic compliance planning. Our findings suggest that while the Omnibus Regulation builds upon established principles, it introduces transformative changes that will fundamentally reshape corporate sustainability practices across Europe and globally.

Introduction

The European Union stands as a global leader in sustainability regulation, continually refining its approach to ensure environmental responsibility and corporate transparency. The EU Omnibus Regulation represents a watershed moment in this journey—an ambitious attempt to streamline existing sustainability frameworks while maintaining their effectiveness.

This paper examines whether the Omnibus Regulation is simply “old wine in a new bottle”—a mere rebranding of existing regulations—or “new wine in a new bottle”—a genuinely innovative approach to sustainability governance. By analyzing its relationship with the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), and the EU Taxonomy for Sustainable Activities, we provide a comprehensive assessment of its impact on businesses within and beyond the EU.

The Current Regulatory Landscape

Corporate Sustainability Reporting Directive (CSRD)

The CSRD represents a significant enhancement over previous non-financial reporting requirements, expanding both scope and substance in sustainability disclosures.

Purpose and Philosophy

The CSRD aims to transform corporate transparency by institutionalizing sustainability as a core reporting obligation alongside financial performance. This reflects the growing recognition that environmental, social, and governance (ESG) factors are material to corporate value creation and risk management.

Comprehensive Scope

EU-listed companies:

All companies listed on EU regulated markets

Large companies:

Entities meeting at least two of three criteria: €40M+ revenue, €20M+ assets, 250+ employees

EU subsidiaries of non-EU companies:

With significant EU operations (€150M+ EU revenue)

Total coverage:

Approximately 50,000 companies, a fourfold increase from previous requirements

Rigorous Requirements

Double materiality approach:

Companies must report on both impacts on sustainability matters and how sustainability issues affect the company

European Sustainability Reporting Standards (ESRS):

Mandatory sector-agnostic and sector-specific standards

Independent assurance:

Initially limited assurance, progressing to reasonable assurance

Digital tagging:

Machine-readable format compatible with the European Single Access Point

Implementation Timeline

January 1, 2024

Large public companies with 500+ employees (FY2024, reporting in 2025)

January 1, 2025

All other large companies (FY2025, reporting in 2026)

January 1, 2026

Listed SMEs, small non-complex financial institutions, and captive insurance companies (with opt-out until 2028)

Corporate Sustainability Due Diligence Directive (CSDDD)

The CSDDD creates a legally binding framework for proactive management of adverse impacts across global value chains.

Purpose and Philosophy

The CSDDD institutionalizes human rights and environmental due diligence as a legal obligation rather than a voluntary commitment. It operationalizes the United Nations Guiding Principles on Business and Human Rights and the OECD Guidelines for Multinational Enterprises.

Strategic Scope

Group 1 companies

Companies must report on both impacts on sustainability matters and how sustainability issues affect the company

Group 2 companies

Non-EU companies with €450M+ EU turnover |

High-impact sectors

Modified thresholds for companies in sectors with heightened risks

Cascading effect

While directly applicable to approximately 5,000 companies, the due diligence requirements cascade through value chains, affecting millions of businesses worldwide |

Core Requirements

Comprehensive due diligence obligation

Identify, prevent, mitigate, and account for actual and potential adverse impacts

Integration into corporate governance

Embed due diligence into policies, risk management, and decision-making processes

Stakeholder engagement

Consultation with affected communities, workers, and other relevant parties

Access to remedy

Establishing grievance mechanisms and providing remediation when appropriate

Climate transition planning

Adoption of science-based plans aligned with the Paris Agreement

Phased Implementation

2027

Companies must report on both impacts on sustainability matters and how sustainability issues affect the company

2028

Non-EU companies with €450M+ EU turnover

2029

Modified thresholds for companies in sectors with heightened risks |

EU Taxonomy for Sustainable Activities

The EU Taxonomy serves as the foundation for the European sustainable finance architecture, providing a science-based classification system for environmentally sustainable economic activities.

Purpose and Philosophy

The Taxonomy creates a common language for sustainable finance, enabling capital markets to identify and support environmentally sustainable investments, thereby facilitating the transition to a low-carbon, resilient and resource-efficient economy.

Universal Scope

- Financial market participants: Including asset managers, institutional investors, and banks

- Large public-interest companies: Subject to CSRD requirements

- EU and Member State authorities: When establishing public measures, standards, or labels

Technical Criteria Framework

Six environmental objectives

- Climate change mitigation

- Climate change adaptation

- Sustainable use and protection of water and marine resources

- Transition to a circular economy

- Pollution prevention and control

- Protection and restoration of biodiversity and ecosystems

Technical screening criteria

Detailed, science-based thresholds and metrics

Do No Significant Harm (DNSH) principle

Activities must not undermine other environmental objectives

Minimum social safeguards

Alignment with international standards such as the ILO Fundamental Conventions

Continuous Development Timeline

2021

Climate Delegated Act (climate mitigation and adaptation)

2022

Complementary Climate Delegated Act (nuclear and natural gas) |

2023

Environmental Delegated Act (remaining four objectives) |

Ongoing

Regular review and refinement of technical screening criteria

The EU Omnibus Regulation: Evolutionary or Revolutionary?

Genesis and Motivation

The Omnibus Regulation emerges from a recognition that while individual sustainability regulations serve valuable purposes, their cumulative effect creates significant compliance challenges. This initiative responds to stakeholder feedback highlighting regulatory overlap, inconsistent terminology, and disproportionate burdens on smaller enterprises.

Transformative Objectives

1. Regulatory Streamlining

The Omnibus Regulation aims to create a coherent sustainability framework by:

- Eliminating redundant reporting requirements across directives

- Harmonizing terminology and concepts

- Creating a unified compliance timeline

- Establishing a centralized data repository

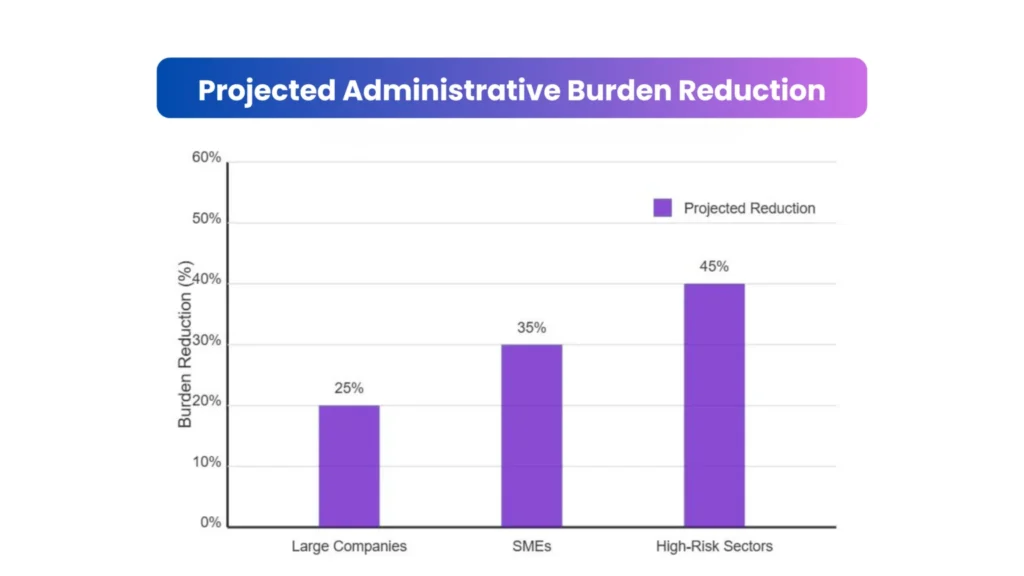

2. Burden Reduction

Concrete targets for administrative relief include:

- 25% reduction in reporting requirements for large companies

- 35% reduction for SMEs

- Simplified verification procedures

- Proportionate implementation based on company size and risk profile

3. Enhanced Effectiveness

Rather than diluting sustainability objectives, the Omnibus approach seeks to enhance effectiveness through:

- Improved data quality through consolidated reporting

- Better resource allocation toward material issues

- Enhanced comparability of sustainability information

- More integrated connection between disclosure and due diligence

Transformative Objectives

1. Integrated Assessment Framework

The Omnibus Regulation introduces a unified approach to sustainability assessment that:

- Connects reporting obligations with due diligence processes

- Aligns impact assessment methodologies with Taxonomy criteria

- Creates a “comply once, report many times” model

- Facilitates interoperability across different reporting frameworks

2. Digital-First Approach

Building on the European Single Access Point (ESAP) initiative, the regulation embraces digital transformation through:

- Standardized machine-readable formats

- Automated compliance checking

- Dynamic reporting capabilities

- Blockchain-based verification options

3. Proportionality Mechanism

Recognizing diverse business realities, the regulation introduces sophisticated proportionality through:

- Risk-based reporting requirements

- Sector-specific materiality guidance

- Simplified standards for non-complex entities

- Progressive implementation pathways

4. Global Alignment Strategy

The regulation positions EU standards within the international landscape by:

- Creating interoperability with ISSB standards

- Establishing equivalence mechanisms for third-country frameworks

- Supporting global convergence through the G7 and G20

- Facilitating mutual recognition arrangements

Company

Our Offerings

Our Offices

Sweden - Ulvsbergsvagen 17B, Tullinge, 14654 Stockholm

India - Lodha Signet 1, Dombivali 421204

Email:

© 2025 All rights reserved.