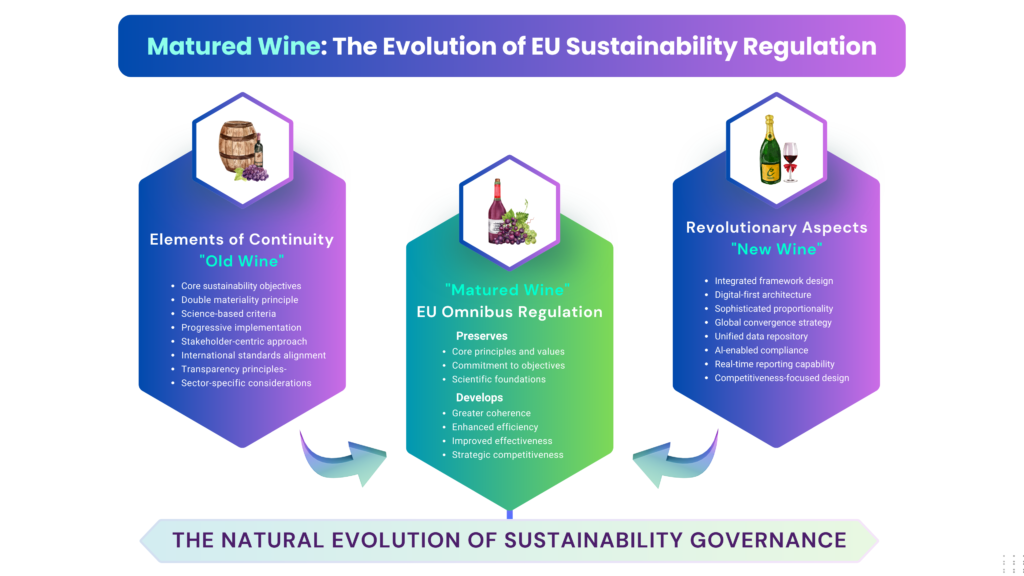

This white paper examines the European Union’s Omnibus Regulation, which represents a pivotal evolution in the EU’s sustainability regulatory framework. By analyzing whether this regulation is merely a repackaging of existing rules or a genuine innovation, we provide stakeholders with crucial insights for strategic compliance planning. Our findings suggest that while the Omnibus Regulation builds upon established principles, it introduces transformative changes that will fundamentally reshape corporate sustainability practices across Europe and globally.